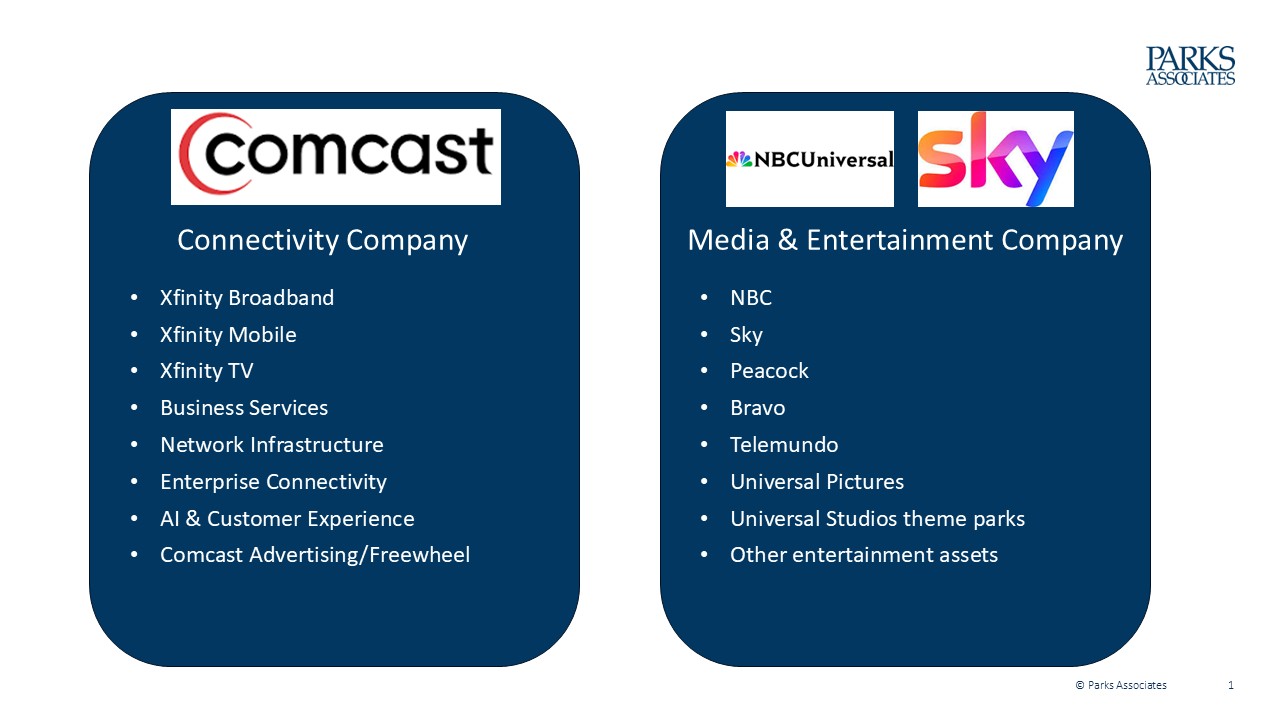

On June 29th, Comcast announced it was going to split into two independent, publicly traded companies, pending regulatory approval, by spinning off NBCUniversal and Sky into a standalone global media and entertainment company while the remaining Comcast focuses on its connectivity businesses. The transaction, expected to close over the next year, is designed to separate two businesses with increasingly different strategic priorities. The new NBCUniversal company will include NBC, Peacock, Universal Pictures, Universal Studios theme parks, Bravo, Telemundo, Sky, and other entertainment assets, while Comcast will retain its broadband, wireless, business services, and connectivity platform operations. Existing Comcast shareholders will receive shares in both companies.

The rationale for spinning out NBCUniversal and Sky is largely strategic.

- The broadband and wireless businesses are largely infrastructure businesses with stable cash flows and investment priorities.

- The media & entertainment businesses operate in a rapidly evolving media landscape shaped by streaming competition, advertising shifts, sports rights inflation, and global content investments.

By separating the companies, management expects each organization to pursue independent capital allocation, partnerships, and acquisitions without being constrained by the other's priorities. Comcast executives have emphasized that the move should create greater operational focus and entrepreneurial decision-making. In addition, the separation also makes NBCUniversal a more flexible participant in future media consolidation.

Implications for Comcast

The planned separation of NBCUniversal and Sky will fundamentally reshape Comcast in a number of ways.

- Sharper strategic focus. Comcast becomes a pure-play connectivity and infrastructure company focused on broadband, wireless, and enterprise services, its highest margin businesses. Comcast can devote more resources to expanding its mobile business, investing in DOCSIS 4.0 and fiber, leveraging AI to improve operations, and developing new connectivity services.

- New role in the entertainment ecosystem. Rather than owning one of the world's largest content portfolios, Comcast becomes a distribution platform that must compete on customer experience, aggregation, and connectivity rather than exclusive programming. This places greater importance on Xfinity's ability to integrate streaming services, simplify content discovery, offer compelling bundles, and leverage broadband and mobile to reduce churn. Success will increasingly depend on being the preferred gateway to entertainment regardless of which content companies’ consumers choose. This puts them into much more direct competition with TV operating system (TV OS) platforms like Roku, Tizen (Samsung), webOS (LG), SmartCast (Vizio), Amazon, and Google.

- Improved capital allocation. Cash previously directed toward streaming losses and media investments can be redirected to network expansion, mobile growth, and shareholder returns.

- Reduced earnings volatility. The company becomes less exposed to cyclical advertising markets, box office performance, and escalating content costs. While simultaneously, its declining pay-TV subscriber numbers will face greater scrutiny.

- Greater emphasis on aggregation. Xfinity must increasingly differentiate through superior content discovery, streaming integration, and bundled broadband-mobile offerings rather than exclusive ownership of content.

- Enhanced strategic flexibility. A simplified corporate structure could improve valuation, reduce the conglomerate discount, and provide greater flexibility for future partnerships or acquisitions in connectivity and technology.

Implications for NBCUniversal and Sky

The spin-off will create a standalone NBCUniversal and Sky with a singular focus on media, streaming, sports, and entertainment.

- Greater strategic independence. Management will gain the flexibility to pursue acquisitions, partnerships, licensing deals, and international expansion without being tied to Comcast's connectivity strategy.

- Increased pressure to deliver profitable streaming. While Peacock has already been moving in this direction, there will be increased expectations toward sustainable profitability, balancing content investment, advertising, pricing, and distribution.

- Sports, already a cornerstone of Peacock programming, becomes an even more valuable strategic asset. NBC Sports, the Olympics, the NFL, Premier League, and Sky Sports become core differentiators for subscriber acquisition, advertising, and platform engagement.

- Sky becomes a larger source of international growth. Sky provides an established European customer base, premium sports rights, and advertising capabilities that can support broader international content and streaming strategies.

- Advertising becomes a primary growth engine. Combining NBCUniversal's premium video inventory with Sky's European advertising business creates opportunities to expand addressable advertising, retail media partnerships, and cross-market campaigns.

- Greater focus on portfolio optimization. Management can more aggressively evaluate which businesses to grow, monetize, or divest, including opportunities to streamline linear networks, expand direct-to-consumer offerings, and optimize the film and television studios.

- Heightened financial discipline. Without Comcast's broadband-generated cash flow, the company must carefully balance investments in content, technology, sports rights, and international expansion while maintaining healthy free cash flow.

- Potential participant in future industry consolidation. As an independent media company, NBCUniversal and Sky could become a more agile acquirer, strategic partner, or merger participant as the industry continues to consolidate around global streaming scale, advertising technology, and premium content. This is particularly relevant as Comcast’s streaming properties have clearly fallen into the second tier of media companies after the Paramount acquisition of Warner Bros. Discovery (WBD) and Fox’s acquisition of Roku, both pending approval.

Broader market implications

The separation of Comcast and NBCUniversal/Sky will have implications well beyond the two companies. It signals a broader shift toward specialization, with connectivity providers and media companies increasingly operating as distinct businesses rather than vertically integrated conglomerates. This could accelerate industry consolidation, reshape content distribution partnerships, and intensify competition in both broadband and streaming.

Traditional Pay TV Operators (Charter, Cox, Altice)

Cable operators will see Comcast competing as a pure connectivity provider rather than a content owner. This is likely to reinforce industry investment in broadband, wireless, and streaming aggregation rather than traditional linear television. Operators may also gain greater flexibility in negotiating carriage agreements with NBCUniversal since Comcast will no longer have the same incentive to use content to support its own distribution business.

As a result, the competitive battleground will shift further toward customer experience, broadband performance, mobile convergence, and content aggregation instead of exclusive programming.

Streaming Platforms (Netflix, Disney, Warner Bros. Discovery, Paramount, Amazon)

A standalone NBCUniversal/Sky becomes a more aggressive streaming competitor. Peacock will have greater incentive to expand distribution, improve monetization, and pursue strategic partnerships that may have been more difficult within Comcast.

At the same time, NBCUniversal could become a more active participant in industry consolidation through acquisitions, joint ventures, or content licensing.

As a result, competition for subscribers, advertising dollars, and premium sports rights is likely to intensify while strategic partnerships become more common.

Smart TV and Connected TV Platforms (Roku, Amazon, Google, Samsung, LG, Vizio)

As Comcast shifts away from owning a major content business, Xfinity becomes increasingly focused on being an aggregation platform rather than promoting proprietary content. This aligns its strategy more closely with TV operating systems that seek to simplify content discovery across multiple services.

Meanwhile, NBCUniversal and Peacock may become more willing to deepen integrations with third-party TV platforms if those relationships accelerate subscriber growth.

As a result, platform neutrality becomes more valuable, creating opportunities for TV OS providers to strengthen discovery, advertising, and commerce partnerships with NBCUniversal.

Content Owners and Sports Leagues

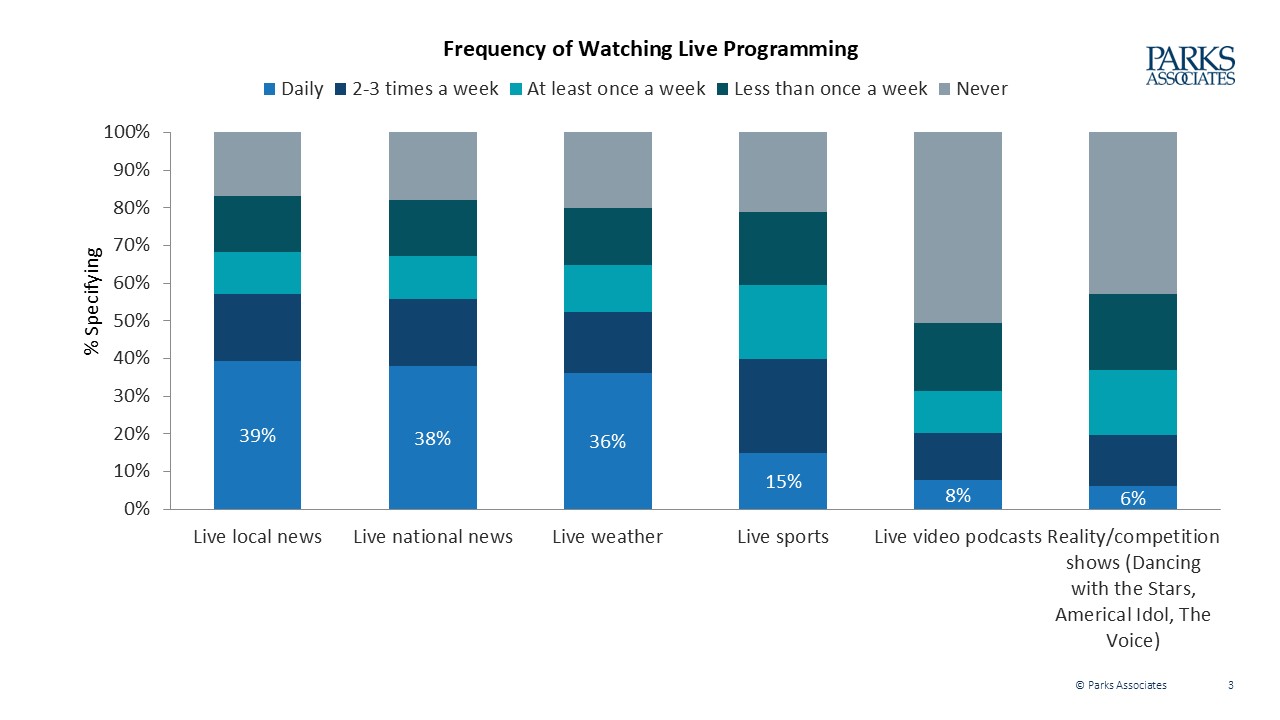

NBCUniversal will likely place even greater strategic emphasis on live sports as one of its primary competitive advantages. This could increase competition for premium sports rights, particularly as rights increasingly support both streaming engagement and advertising. Parks Associates research shows that live sports is one of the few categories that drives habitual viewing, with 40% of viewers watching live sports at least two to three times per week. That recurring engagement makes sports especially valuable for subscriber retention, advertising inventory, and platform differentiation.

Studios and independent content producers may also benefit from a greater willingness by NBCUniversal to license content externally if it improves financial returns. As media companies place greater emphasis on programming that consistently drives audience engagement, entertainment content may increasingly be evaluated based on its ability to maximize licensing revenue across multiple distribution platforms.

As a result, premium sports rights will become even more valuable, while content licensing strategies may become more flexible. For sports leagues and content owners, this environment is likely to create greater competition for exclusive rights as broadcasters and streaming providers continue to invest in live programming that builds long-term viewer loyalty.

Advertisers and Ad Tech Companies

A standalone NBCUniversal/Sky is likely to accelerate investment in advertising technology (particularly since Comcast is keeping Comcast Advertising and Freewheel), audience measurement, retail media partnerships, and cross-platform targeting. With advertising becoming a larger contributor to future growth, NBCUniversal has strong incentives to maximize the value of its premium video inventory.

As a result, demand for unified measurement, identity solutions, commerce media, and advanced CTV advertising capabilities is likely to increase.

Broadband Competitors

Companies such as Verizon, T-Mobile, Frontier, and AT&T will face a Comcast that is singularly focused on connectivity. Expect increased investment in network performance, fixed wireless competition, converged broadband-mobile bundles, and AI-driven customer service.

As a result, competition will further shift toward network quality, pricing, and bundled connectivity services rather than video offerings.

The proposed separation of NBCUniversal's cable networks reflects Comcast's broader shift toward a connectivity-focused business. As media assets become less central to the company's strategy, improving broadband customer satisfaction and expanding higher-value services, including home security and smart home offerings, will be critical to strengthening customer loyalty and reducing churn.

Key Takeaways

The Comcast-NBCUniversal separation represents the next phase of media industry restructuring. Over the past decade, many companies pursued vertical integration to combine distribution with content. Today, the market is increasingly rewarding focused business models that allow each company to optimize its own economics and strategic priorities.

- Accelerates industry specialization as telecom infrastructure and media/content businesses become increasingly independent.

- May trigger additional consolidation among media companies seeking greater scale in streaming, advertising, and sports.

- Raises the strategic value of sports rights, which remain one of the few categories that consistently drive both subscriber acquisition and advertising revenue.

- Strengthens the role of aggregation platforms, including TV operating systems and broadband providers, as consumers continue to assemble entertainment from multiple streaming services.

- Increases competitive intensity in CTV advertising, with NBCUniversal expected to invest more aggressively in advertising technology, measurement, and commerce capabilities to compete with Netflix, Amazon, YouTube, and Disney.