On February 26, 2026, Netflix formally pulled out of its planned acquisition of Warner Bros. Discovery (WBD) after a rival bid from Paramount Skydance emerged that the WBD board deemed financially superior. Netflix had agreed in late 2025 to buy WBD’s studio and streaming assets, including Warner Bros., and HBO Max, but excluding its cable assets, for about $82.7 billion.

Paramount Skydance’s initial bid for Warner Bros. Discovery (WBD) was an all-cash offer aimed at buying the entire company for about a $108 billion, Paramount argued that its proposal provided greater certainty and more immediate value to WBD shareholders because it was entirely in cash, covered all of WBD’s assets (including cable networks and news channels), and avoided the regulatory complexities and stock risk associated with Netflix’s deal.

At the time. Warner Bros. Discovery rejected Paramount’s offer because its board concluded the bid did not provide sufficient value or certainty for shareholders compared with its agreement with Netflix, judging Paramount’s proposal inferior across key criteria, such as value delivered, financing certainty, and likelihood of closing successfully. The board also highlighted risks and costs associated with Paramount’s offer, including additional expenses like termination and interest costs that could reduce net value to shareholders.

Paramount sweetened and revised its bid to over $110 billion, with added incentives such as a ticking fee, a $7 billion regulatory termination payment, and covering the breakup fee WBD would owe Netflix (reported to be roughly $2.8 billion) if the deal fell apart. The WBD board ultimately determined Paramount’s revised proposal could reasonably be expected to be a superior proposal prompting Netflix to step aside. Paramount’s bid now stands as the likely path forward, pending regulatory and shareholder approvals.

Implications for Paramount

The video marketplace is fragmented, necessitating that media companies take an ecosystem-driven approach in deploying content across multiple platforms. Embracing multiple distribution platforms (i.e., film, broadcast, pay TV, SVOD, FAST, AVOD) and business models (i.e., licensing, subscription, advertising, transactional) to maximize reach and corresponding revenues.

Pending regulatory and shareholder approval, Paramount’s acquisition of Warner Bros. Discovery would be transformational, creating one of the largest diversified media companies in the world. The combined entity would control an enormous portfolio of film studios, premium TV brands (including HBO Max), broadcast networks, cable channels, and streaming platforms, significantly expanding Paramount’s scale in both content production and global distribution.

Today the three biggest media companies (Google, Amazon, and Disney) reach nearly 6 out of 10 consumers via their various platforms. Assuming Paramount successfully completes the acquisition of WBD without any significant divestures, the combined company will reach 57% of US broadband households, putting it on par with Netflix, Amazon, Google, and Disney in terms of reach.

In addition to extending Paramount’s reach the acquisition of Warner Bros. Discovery brings a number of other tangible benefits.

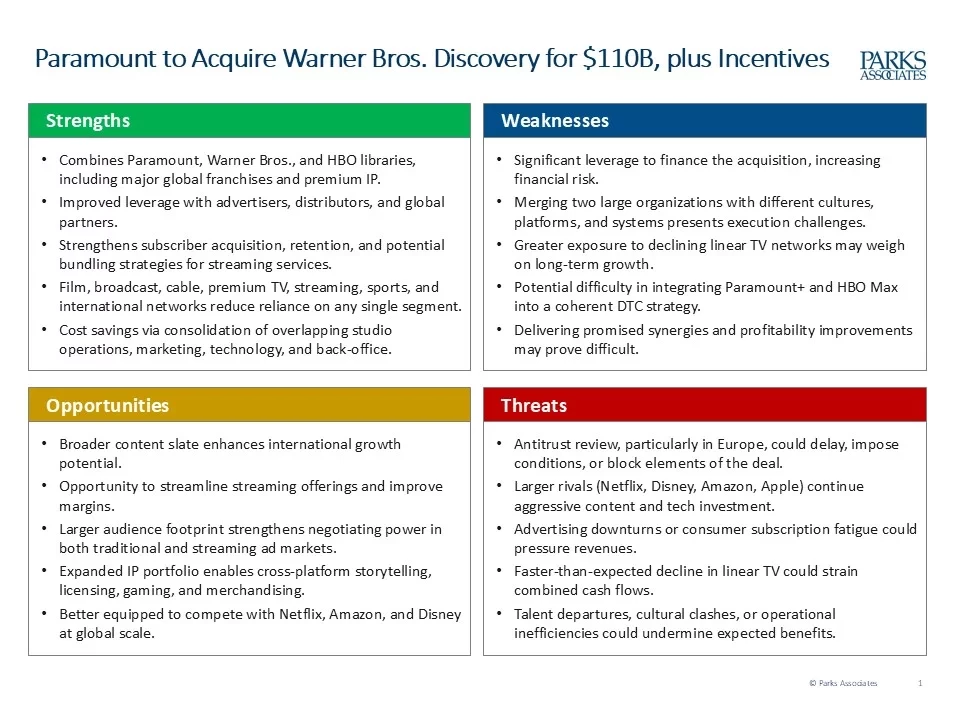

- Expanded premium IP & franchises. Adds HBO Max, Warner Bros. Studios, some of the most globally recognized franchises in entertainment, including Harry Potter, Friends, The Big Bang Theory, Game of Thrones, and the DC Universe to Paramount’s portfolio. In addition, it will enable cross-platform monetization across film, streaming, television, licensing, gaming, and consumer products.

- Strengthened streaming proposition. This acquisition strengthens Paramount’s streaming economics by combining Paramount+ and HBO Max into a deeper, more competitive direct-to-consumer offering with significantly expanded premium content. A larger, more diverse library can improve subscriber acquisition and retention while supporting stronger pricing power and reduced churn. Greater scale also enhances advertising revenue potential in ad-supported tiers and allows content costs to be spread across a broader subscriber base, improving margins and accelerating the path toward sustained streaming profitability. In addition, this acquisition expands Paramount’s global direct-to-consumer (DTC) footprint.

- Scale drives leverage. Paramount’s acquisition of WBD will create one of the largest global media companies by reach, revenue, content library, and production capacity. By combining premium IP, global distribution networks, sports rights, and streaming platforms, Paramount would move from being one major player among several to becoming a consolidated content powerhouse, improving its negotiating position across advertising, distribution, and international markets.

- Global expansion capability. The acquisition significantly strengthens Paramount’s global expansion capability by adding WBD’s established international distribution infrastructure, regional networks, and globally recognized brands like HBO and Warner Bros. This broader footprint enhances Paramount’s ability to scale streaming services internationally, secure co-production partnerships, negotiate licensing agreements, and monetize franchises across diverse markets. With deeper content libraries and stronger brand equity, the combined company would be better positioned to accelerate subscriber growth, increase international advertising opportunities, and compete more effectively in key global regions.

The deal, however, does not come without significant risk.

- Balance sheet & capital structure risk. The acquisition will increase leverage significantly. Elevated debt levels reduce financial flexibility and heighten exposure to cyclical advertising declines, box office volatility, and macroeconomic slowdown. Rapid deleveraging and synergy realization will be critical.

- Integration & execution risk. Combining two large organizations, across studios, streaming platforms, networks, technology infrastructure, and leadership, introduces substantial operational complexity. Delays, cultural misalignment, or talent attrition could erode anticipated cost and revenue synergies.

- Linear TV decline. The combined entity increases exposure to legacy cable networks amid accelerating cord-cutting trends. Managing cash flow from declining linear assets while scaling streaming profitability will require careful capital allocation.

- Regulatory & competitive risk. Antitrust scrutiny could delay closing or impose structural conditions. While this deal is less likely to receive significant scrutiny from US regulators this will not be the case in Europe where it is likely to face intense scrutiny. Additionally, competitors may respond aggressively through pricing strategies, content spending, or strategic partnerships.

The SWOT Analysis below gives further insight into the opportunities and challenges that accompany the merger of Paramount and Warner Bros. Discovery.

Implications for Netflix

Netflix’s decision to walk away from the Warner Bros. Discovery acquisition preserves its balance sheet and avoids taking on significant debt and integration risk at a time when large media mergers face intense regulatory scrutiny. While the deal would have dramatically expanded Netflix’s content library and studio footprint, backing out allows the company to maintain strategic flexibility, continue investing in original content, gaming, advertising, and live programming, and avoid the operational complexity of absorbing a legacy media conglomerate.

Financially, receiving a substantial breakup fee (reported to be $2.8B) softens the impact of the failed deal. Strategically, however, Netflix remains a single service company, though one that reaches 64% of US broadband households and forgoes the opportunity to control major franchises and premium brands like HBO Max, Harry Potter, Friends, The Big Bang Theory, Game of Thrones, and the DC Universe. It will need to compete against a potentially larger, combined Paramount/WBD entity with an even deeper catalog.

The outcome reinforces Netflix’s position as a focused, streaming-first company rather than a diversified legacy media operator.

- Preserves Netflix’s financial flexibility. Avoids a massive cash outlay and potential debt burden tied to acquiring WBD.

- Demonstrates capital discipline. Reinforces investor confidence after declining to overpay in a bidding war.

- Receives a sizable breakup fee, reported to be $2.8B. This provides additional capital for content, live programming, advertising, share repurchases or a different acquisition.

- Avoids integration risk. History is riddled with failed mergers associated with the challenges associated with absorbing a large, complex legacy media company.

- Maintains strategic focus. Netflix will continue to be a pure-play, streaming-first global platform rather than a diversified legacy media conglomerate.

On the downside Netflix is faced with the following challenges.

- Netflix misses out on premium assets. Acquiring HBO Max and major film and TV franchises would have significantly strengthened Netflix’s content moat.

- Netflix faces a stronger competitor. Assuming regulatory and shareholder approval and the successful integration of the two companies, Netflix will face a much stronger competitor than if it was competing with them separately.

Implications for the Market Overall

The collapse of Netflix’s bid and Paramount’s move to acquire Warner Bros. Discovery underscores accelerating consolidation across the media and streaming landscape. As scale becomes increasingly critical to compete globally, the emergence of a combined Paramount/WBD intensifies competition with Netflix, Disney, and other major platforms by concentrating premium content, franchises, and distribution under fewer corporate umbrellas. This dynamic raises the competitive bar for mid-sized players, potentially pushing them toward partnerships, mergers, or strategic realignments to remain viable.

At the same time, the situation highlights growing investor emphasis on disciplined capital allocation and sustainable streaming economics rather than expansion at any cost. A larger Paramount/WBD entity could reshape content licensing by keeping more premium programming in-house, further fragmenting the streaming ecosystem. The deal also reinforces the broader industry shift away from legacy cable toward DTC models, with consolidation serving as a mechanism to manage declining linear revenues while pursuing streaming profitability.

Key implications for the market include the following.

- Intensified streaming competition, particularly if a combined Paramount–WBD strengthens its direct-to-consumer offering.

- Increased pressure on mid-sized media companies to seek partnerships or mergers to remain competitive.

- Heightened regulatory focus on media concentration, vertical integration, and control of premium content, particularly in the EU.

- Shifts investor sentiment toward disciplined M&A, rewarding companies that avoid overpaying in bidding wars.

- Rebalances content licensing dynamics, as more premium content may be kept in-house rather than licensed externally.

- Continued decline of legacy cable, with consolidation used as a strategy to manage shrinking linear TV revenues.

Conclusion

Parmount’s proposed acquisition of Warner Bros. Discovery is transformational, creating one of the largest global media and entertainment companies with unmatched breadth across film, television, sports, news, and streaming. The combined entity materially strengthens competitive positioning against Netflix, Disney, Amazon, Comcast, Google, and Apple through expanded IP ownership, global scale, and diversified revenue streams.

However, the transaction carries significant financial, operational, and execution risk. Whether the acquisition proves successful or will be yet another failed merger among major media companies will depend less on strategic rationale, which is strong, but more on disciplined integration, speed of execution, capital allocation, and a clearly defined post-merger operating model.